Cryptocurrencies in India. Risks of the lack of regulation framework

According to the International Monetary Fund, India the world's fifth size economy in terms of GDP and first in terms of population, being one of the largest emerging economies in the world. India is also one of the countries where the use of cryptocurrencies is becoming more widespread despite the lack of comprehensive regulation framework. According to the Chainalysis report the adoption of cryptocurrencies by citizens of India is at one of the highest levels among emerging economies, second only to Vietnam, as evidenced by the constant growth in the number and volume of cryptocurrency transactions, especially those made by individual users.

The volatility of the national currencies of emerging economies and the desire of their citizens to save their savings are traditional reasons for the popularity of cryptocurrencies in these countries. In India, the government has been actively pursuing a policy of digitalizing the economy and making digital services more accessible to the public, starting with the launch of the Aadhaar program in 2009 and following with financial program PMJDY in 2014. The widespread adoption of digital financial services driven by government support has also moved forward the rapid growth of cryptocurrencies and related services adoption in the country.

The official position of the Indian authorities regarding digital assets has undergone several changes in recent years. Initially, RBI - the Central Bank of India had a negative attitude towards digital currencies, up to its ban in 2018. The Supreme Court of India later overturned this RBI decision. The court stated that noted that in the absence of any legislative ban on the buying or selling of cryptocurrencies, the RBI cannot impose disproportionate restrictions on trading in these currencies. The court felt such restrictions would interfere with the fundamental right of citizens to carry out any trade that is deemed legitimate under the law.

By now, India has neither a ban on the use of cryptocurrencies (or crypto assets), nor any special regulation of their actual turnover. There is a “Cryptocurrency and Regulation of Official Digital Currency Bill, 2021” under consideration in the Parliament of India, which has been essentially discussing since 2018 and there is no understanding of when it will be passed, as the Central Bank of India believes that cryptocurrencies represent a threat to financial stability. In its current form, most likely, the bill will create a legal basis for issuing a state digital currency (CBDC) and promoting blockchain technology and its use.

At the same time, starting April 2022, all transactions with cryptocurrencies in India are taxed at 30%, as before gambling or other speculative transactions. Also, from July 1, TDS of 1% came into effect for virtual currency payments over 10,000 rupees per year. In the future, this fee will be able to highlight the government of those who carry out trading operations with cryptocurrency.

The hesitation in adopting regulation, as in other countries where there is still no legal framework for the cryptocurrency, is most likely due to security concerns and cryptocurrency-associated risks. Regulators try to avoid cryptocurrencies because of money laundering, terrorist financing, and scam threats.

Nevertheless, back in 2018, the Financial Action Task Force on Money Laundering (FATF) issued guidance on compliance with anti-money laundering standards for virtual asset service providers. The guidance was updated in 2021 and includes requirements for identifying customers and reporting information about cryptocurrency transactions. Compliance to this guideline can greatly reduce all mentioned risks.

Many countries already have implemented these mechanisms for minimizing risks of using of crypto assets. At the same time, in countries where there is still no comprehensive regulation, cryptocurrencies continue to be a tool for committing crimes. Some time ago we wrote about the biggest scam in Turkey, based on the Ponzi scheme, when more than 2 billion dollars was stolen.

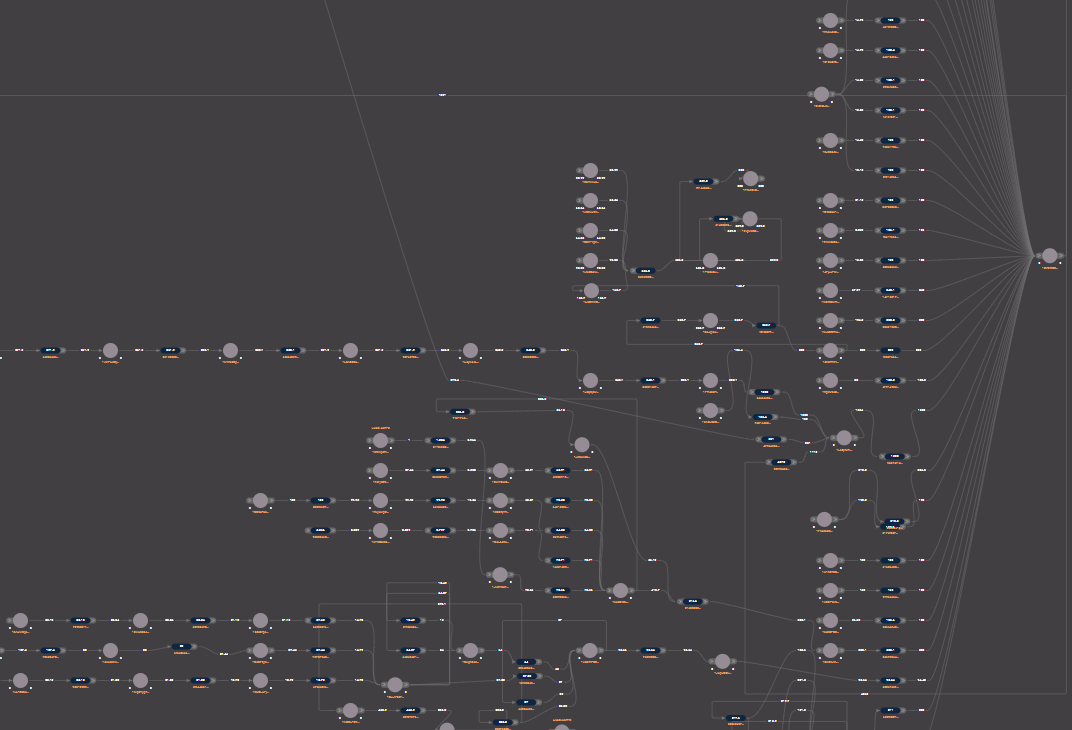

In India scammers often use cryptocurrency to deceive gullible customers as well. There are various criminal schemes such as fake crypto exchanges, where you can lose $100 or a large-scale financial pyramid, such as GainBitcoin, which is considered to be one of the largest cryptocurrency Ponzi schemes in the world, where about 100,000 people suffered and more than 300 thousand bitcoins were stolen.

The TokenScope Team, set itself the task to investigate the circumstances of the theft of GainBitcoin project participants. This large-scale investigation is currently underway and will soon be completed and revealed. Follow us.